Private Credit News Weekly Issue #101: Everyone Sold First. The Losses Come Later.

Private Debt News reaches institutional investors, credit professionals, and LP decision-makers. Early sponsor rates available. Contact us here or reply directly to this email.

A fun thing about financial conferences is that nobody flies to Berlin to announce that everything is fine. If everything were fine you would stay home and collect your spread. And yet the private capital industry gathered at SuperReturn this week to tell each other, at considerable length and expense, that everything is fine. The reassurance speech is a genre that only exists because somebody needs reassuring, and this week the speeches came with an unusually specific list of things not to worry about, which is generally how you find out what people are worried about.

The list, this year: software, redemptions, valuations, and data centers. Let’s take them in order.

The Word in the Deal Memo

Here is a stylized history of private credit. For about a decade, the best thing you could possibly lend against was enterprise software. The revenue recurred. The customers never left. Lenders did not so much underwrite software companies as underwrite the word “software,” which appeared in the deal memo, which was sufficient. Everyone made money and the category got bigger and bigger.

Then AI arrived, investors started worrying that the borrowers might be made obsolete, software-heavy funds saw outflows, and the asset managers responded the way asset managers respond, which is with frameworks.

Apollo now screens every new software investment for AI disruption risk. Their thematic team built a system last year that carves software into 12 to 14 categories, ranks each by susceptibility to AI, and then, this is the interesting part, they ran the framework backward over the existing portfolio to figure out what to exit. Rob Bittencourt, who runs thematic investing there, calls AI probably the most profound platform shift the industry has faced, says workflow-replaceable software (he cites data visualization) is most at risk, and notes that regulated sectors like healthcare are insulated precisely because they are too encumbered to adopt anything quickly. The framework also grades management on whether they articulate strategic vision with sufficient urgency. Soft factors, he concedes. When your credit screen includes a vibes assessment of the CEO’s urgency, you are admitting the spreadsheet no longer captures the risk.

Apollo is not alone. Ares hired an outside consultant to examine the software in its biggest public private credit fund. Blackstone and Blue Owl ran internal reviews. Silver Lake built a twenty-person internal AI team to educate its own dealmakers. The entire industry essentially re-underwrote itself in about a year, which is impressive, and also tells you how confident everyone was in the original underwriting.

The bulls and bears then divide neatly by exposure. Victor Khosla of SVP, who has zero software, says software businesses that get into trouble don’t get into a little trouble, they fall off a cliff. Fortress expects lower recoveries and harsher losses on software loans made in 2020 and 2021. Carlyle’s John Redett reports that LPs no longer want to hear about software at all; they want industrials, defense, energy, supply chains. “The old world is the new world,” as he put it, which is a sentence that would have gotten you laughed out of a 2021 LP meeting. Meanwhile Goldman’s asset management arm says software is among its best performing sectors, James Reynolds notes that not all software is created equal, and Orlando Bravo, whose firm has rather a lot riding on the answer, declared the SaaSpocalypse finished. It is perhaps worth noting that Bravo also said Thoma Bravo is treading carefully on new tech deals because it wants to buy companies that are part of the future. The apocalypse is over but we are being careful, is a posture.

A Reckoning With a Date on It

Normally credit problems are vague. “There will be losses someday” is not a trade. What makes this cycle unusual is that it comes with dates.

Brook Hinchman at Oaktree counts more than $200 billion of high yield and leveraged loan debt trading below 90 cents and yielding north of 15%, mostly out of the 2021 and 2022 buyout vintages. His argument is about arithmetic, not technology. Struggling companies responded to higher rates with PIK debt and liability management exercises, there has been, in his words, a lot of kicking of the can, but loans run about six years, and six years after 2021 is, well. You can do the math. Once borrowers hit hard maturities the options run out, which for Oaktree is not a warning but a pipeline.

Citi’s strategists supplied the schedule: roughly a third of tech issuers with 2028 maturities have not demonstrated capital markets access in years, and those companies start attempting refinancings in the second half of 2026. Which is to say, now. Pimco’s CIO says the first sustained default cycle in years has already begun. The distinctive feature of the moment is that the lenders dreading the maturity wall and the distressed funds celebrating it have circled the same quarters on the same calendar.

And the private equity sellers feeding all this are, by their own description, stuck. Khosla again: entire sectors, PE and real estate among them, are “constipated” and can’t sell. Apollo’s Scott Kleinman says the industry lost its way during the zero-rate decade, the 2017 to 2022 fund vintages are the strugglers, the inventory of PE-owned companies is really high, and firms will have to start capitulating on valuations, with some managers shrinking or disappearing outright. There is capital available for exits, he notes, you just may not like the price. That is the entire private markets problem in one sentence.

Performing Exactly as Intended

Blackstone’s BCRED, the largest fund of its kind, limited redemptions to 5% last week. Blue Owl’s OCIC, a $37 billion vehicle, got withdrawal requests for more than 20% of its shares earlier this year and capped them at 5%, along with its sister tech fund. Partners Group is curbing redemptions too. The pattern is non-traded BDCs, retail and wealth money, software exposure, in roughly that causal order.

The industry’s defense is worth hearing out. Ares’ Blair Jacobson says the wealth vehicles are performing exactly as intended and the underlying credit statistics are actually improving; the problem is the psychology of individual investors, not the portfolios. Goldman’s Reynolds points out that non-traded BDCs are a sliver of an asset class that broadly defined could run to $30 or $40 trillion. Fine. But “the product works, the customers are panicking” is a strange flex for a product that was sold to those exact customers on the premise of stability, and the tell is what the gated funds are doing next: OCIC went to the investment grade bond market this week and raised $500 million, at a healthy spread, partly because, as one analyst put it, demonstrating ongoing access to debt capital markets sends a constructive signal. You issue bonds to repay debt. You also issue bonds to prove you can.

Sixth Street’s Julian Salisbury, refreshingly, skipped the reassurance entirely: he expects defaults across private credit to rise, given how fast the industry ballooned to $1.8 trillion, and when things grow this fast there will inevitably be losers.

The most clarifying voice of the week came from Stockholm, of all places. Erik Fransson, who gatekeeps which funds Swedish pension savers can buy, was asked whether private markets belong in the country’s premium pension system and just said no. Private market structures with daily liquidity are usually a recipe for difficulties, very few individuals can evaluate the risk-return tradeoff, and even if you could engineer daily valuation, he doubts the structure survives a stressed market. This, at the precise moment US regulators are working to ease private equity and private credit into 401(k)s. The Swedes looked at the product and read the label.

Twice as Likely to Lose

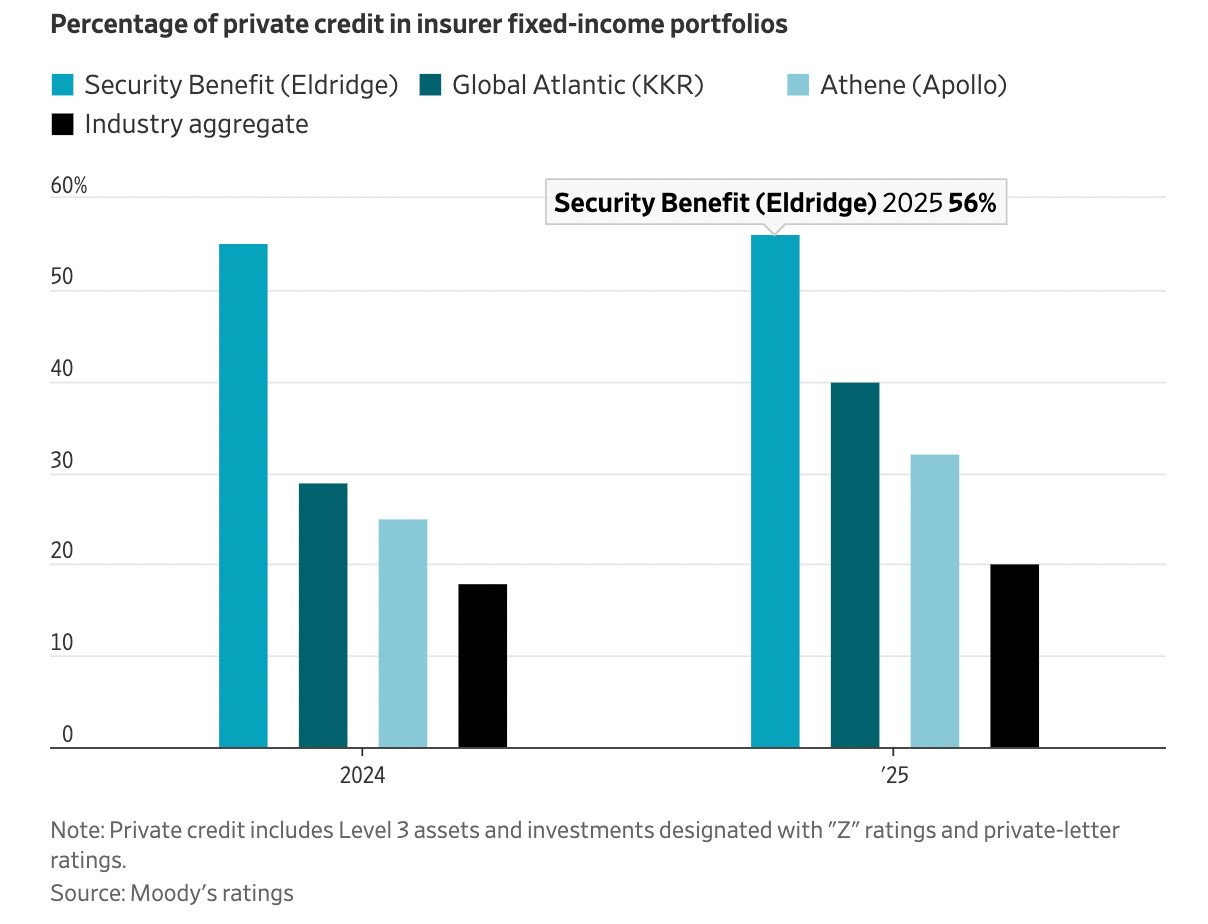

While we are on the subject of labels. Researchers at Columbia Business School (Li, Oh, and Ricciardi) studied the private letter ratings that US life insurers increasingly rely on and found that a privately rated bond is roughly twice as likely to suffer a credit loss as a publicly rated bond carrying the identical grade. A private BBB-, in other words, behaves like public junk. The gap conveniently disappears for bonds that also carry a public rating, and the authors find evidence consistent with insurers using private ratings strategically for capital relief, to the tune of about $4.5 billion a year in avoided capital charges.

Now layer on Moody’s numbers from this week: US life insurers grew their private credit holdings 18% in a year, to $807 billion. A fifth of the industry’s $4 trillion in fixed income is now illiquid. ABS ran 38% of 2025 purchases versus 27% of existing holdings, meaning the new money is going into the harder-to-model stuff. Moody’s calls the shift structural, not cyclical. So: structurally growing exposure, measured with ratings that systematically understate risk, generating capital relief on the order of billions. Each piece of this is individually defensible and the combination is how you build a problem nobody owns. The fun part about capital is that nobody checks until they have to.

Where the Money Runs

Where is the money going instead? A few places, each with its own logic and its own irony.

Europe, where Apollo is hiring for a whole new lending platform aimed at small and mid-sized businesses, hoping to originate billions of euros a year, and where Eurazeo just raised €3.9 billion and Bridgepoint is closing in on €5 billion. The pitch is explicit: Europe has less retail money and less software, i.e., fewer American problems. Jim Zelter has talked about $100 billion of deployment in Germany alone over a decade.

Emerging markets, where the pitch is even blunter. Ninety One’s credit team argues the US quietly became a borrower’s market while everyone felt safe in it, whereas EM remains a lender’s market: covenant-lite doesn’t exist, unsecured doesn’t exist, leverage runs three to four turns instead of six or seven, and you collect 150 to 200 extra basis points for roughly one point of extra default risk with recoveries north of 70%. Whether you believe the GEMs data or not, the structural point stands. Protections migrate to wherever capital is scarce, and capital has not been scarce in US direct lending for a long time.

And data centers, the destination for the biggest dollars of all, where Salisbury offered the gentle observation that there is no functioning market yet for selling a finished, stabilized data center, that lenders are competing to fund the same handful of borrowers, that the capital needs are on a magnitude nobody has seen, and that he expects some kind of shakeout within two to four years. Franklin Templeton’s CEO and Howard Marks have separately mused about obsolescence risk. So, to recap: the industry is rotating out of software, an asset with a troubled but at least observable secondary market, into an asset with no exit market at all, financed at a scale without precedent. This is presumably fine. (The week’s number: $35 billion, the financing package Apollo and Blackstone just finalized for Anthropic’s AI infrastructure. The same firms screening their portfolios for AI disruption are funding the disruptor. Both legs of that trade can be rational. It is still a remarkable straddle.)

Seawalls Before the Tide

The one-sentence version of this entire week is that positioning has moved faster than losses.

Everyone built a framework. Everyone gated. Everyone hired the consultant, ran the screen, re-graded the book. The seawalls went up with impressive speed, and the tide has not come in. Defaults haven’t accelerated, by the industry’s own telling. The marks haven’t moved much. The 2021 vintage hasn’t hit its wall.

It will, on roughly the schedule everyone in Berlin already agrees on, which is the strange comfort of the moment: rarely has a reckoning been this well-attended in advance. Refinancing attempts start this half. Hard maturities follow. The winners will be the lenders who can actually tell one kind of software from another, and the buyers waiting patiently on the other side of the gates.