Private Credit News Weekly Issue #96: Banks Tighten the Screws, $770 Billion in Stress, and Private Equity Has It Worse

Back leverage costs are rising, disclosure demands are growing, and the real reckoning may not be in credit at all

Sponsorship: Private Debt News reaches institutional investors, credit professionals, and LP decision-makers. Early sponsor rates available. Contact us here or reply directly to this email.

The tone shifted this week. Not dramatically. But the first quarter bank earnings provided something the private credit market hasn’t had in months: a moment to breathe. Blue Owl’s stock posted its biggest two-day gain since 2022. PIMCO bought a $400 million Blue Owl bond outright, the first BDC unsecured debt deal in over a month. Goldman followed with a $750 million offering of its own. More are expected.

The redemption wave hasn’t stopped. The structural problems haven’t been solved. But the acute panic that defined March appears, for now, to be easing.

What replaced it this week was something more interesting. The banks started talking.

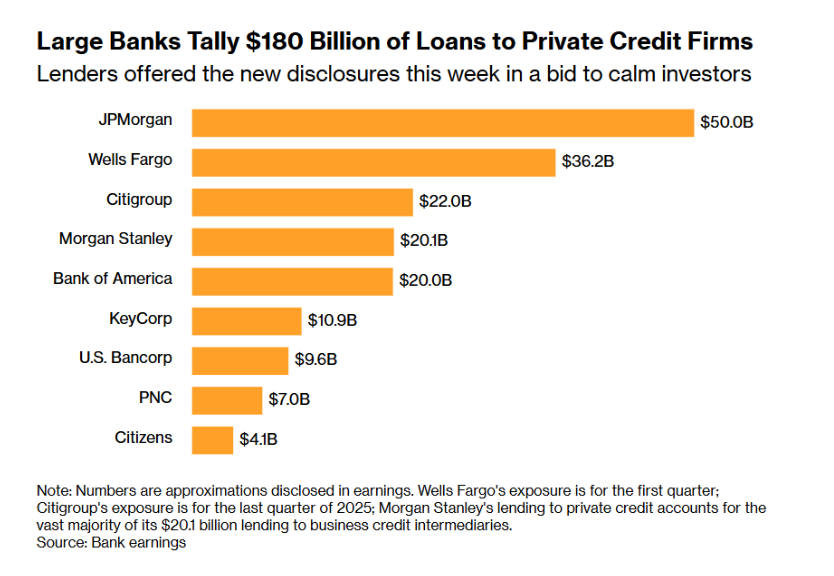

$180 Billion and Counting

For years, the precise scale of Wall Street’s exposure to private credit was a matter of estimates and inference. This week, under pressure from investors and the Federal Reserve, the major banks disclosed it directly.

JPMorgan: $50 billion. Wells Fargo: $36.2 billion. Citigroup: $22 billion. Morgan Stanley: $20.1 billion. Bank of America: $20 billion. Total across the nine banks that disclosed: roughly $180 billion.

The executives were uniform in their reassurance. Jamie Dimon said “you have to have very large losses in private credit before at least it looks like banks are going to get hit.” Morgan Stanley CEO Ted Pick called private credit “an adolescent moment” and said it “will perform broadly in line with the economy.” Wells Fargo CFO Michael Santomassimo pointed to decades of lending experience and structural protections.

The disclosures were designed to calm investors. They mostly succeeded on that narrow goal. But read carefully, they revealed something else.

The $180 billion figure is what banks disclosed voluntarily, with definitions that vary across institutions. Bank of Montreal told analyst Darko Mihelic at RBC that its private credit lending was about 1% of its overall book. Mihelic’s own calculations put it at closer to 7%. Canada’s bank regulator restored non-bank lending to its annual risk report this week after a three-year hiatus, citing concerns that “opaque” markets and high leverage could intensify losses in a crisis.

The transparency push that produced this week’s disclosures is just beginning. It won’t stop here.

Banks Are Tightening Back Leverage Quietly

The disclosure story is the one that ran in headlines. The more consequential story ran underneath it.

Behind the scenes, major banks are tightening their back leverage arrangements with private credit funds. JPMorgan, Goldman and Barclays are exercising their rights to mark down individual loans posted as collateral, prompting fund managers to swap out assets from collateral pools. Back leverage rates are rising, with some now topping 3 percentage points over SOFR, up 50 to 150 basis points from prior levels. Top bank executives are getting directly involved in adjusting rates and collateral terms.

This isn’t new behavior. JPMorgan has done broad-based markdowns in 2022 and twice in 2020. What’s new is the prevalence. The strategies banks are employing to protect themselves are becoming more common across more facilities simultaneously.

The mechanics matter. When a bank marks down collateral, the fund can respond in a few ways. Borrow less. Post more equity. Or swap out the marked asset for something the bank finds more acceptable. That last option is the most common, and it means assets that one bank has flagged as problematic are potentially moving into collateral pools at other banks.

JPMorgan charges lower rates but demands stronger unilateral marking rights. Other banks have dispute provisions and third-party arbitration built into their facilities. The inconsistency across arrangements means banks don’t all have equal protection, and some may find themselves better positioned than rivals if defaults begin to rise.

The return compression is the immediate practical consequence. Funds that built return projections on back leverage at SOFR plus 150 now face SOFR plus 300. That gap has to come from somewhere. Either the fund demands wider spreads from borrowers, which is happening at the margin, or the returns get thinner, which pressures distributions, which generates redemption demand.

The cycle is self-reinforcing and it’s running quietly in the background of every earnings call reassurance this week.

The $770 Billion Number Nobody Wants to Own

The most sobering data point of the week didn’t come from a bank or a fund manager. It came from Davidson Kempner partner Suzy Gibbons.

About a third of the direct lending market is currently stressed, Gibbons said on the Credit Edge podcast. On basic fundamental credit metrics, including changes in leverage versus earnings and interest coverage ratios, roughly $770 billion of loans to US companies are already in troubled territory. That’s double the stressed level at end-2019. If you tighten the screen to companies exceeding 7x earnings, the number is closer to 40% of the market.

Gibbons was careful to distinguish between stressed and defaulted. An acute crisis is unlikely, she said. But soft defaults will mutate into hard defaults. And when they do, recovery rates will probably surprise people.

The data on recovery rates is worth sitting with. Average recovery rates in the leveraged loan market fell to 36 cents in 2025 from around 60 cents a decade ago. Gibbons said she has “no reason” to think private credit recoveries will be stronger. The starting leverage in this cycle is higher than prior cycles. The PE owners backstopping many of these credits are running out of road on extend-and-pretend.

Adams Street Partners’ Jeff Diehl made a related point from a different angle. Current disclosure standards for private credit funds are incomplete, he said, and need to change. Beyond non-accrual rates and PIK percentages, Diehl wants funds to disclose the percentage of assets in loans above 60% LTV, the percentage where interest costs exceed pre-tax cash flows, and the percentage above 6x pre-tax cash flows. His warning thresholds: 10%, 5% and 20% respectively.

The argument is straightforward. Managers with material cushion to those thresholds are probably fine. Managers near or through multiple thresholds are not, even if current marks and yields look acceptable. The NAV doesn’t tell you that story. The additional metrics would.

Apollo has said it’s working toward monthly NAV reporting and eventually daily NAVs with third-party valuations. That’s the direction the industry needs to move. The question is whether it moves voluntarily or gets pushed by regulators who are now clearly paying attention.

Private Equity Has It Worse

The private credit stress has been the dominant story for months. Chris Bryant at Bloomberg Opinion made the case this week that it might be the wrong place to look.

Private credit managers have a genuinely persuasive defense: their loans are senior secured. In a typical software buyout, PE contributed more than half the purchase price as equity. The asset value would need to fall 60-70% before senior secured lenders take losses. The equity cushion absorbs the first hit.

That’s the good news for credit. The bad news is what it implies for PE.

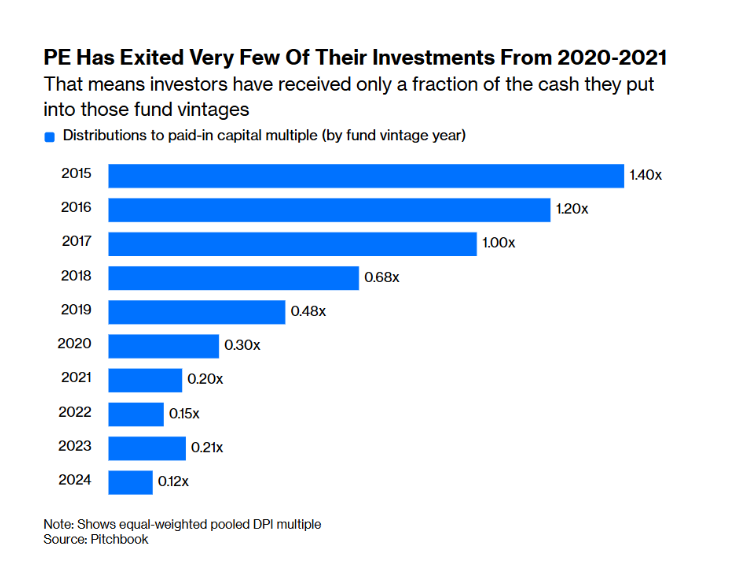

Private equity firms are sitting on a massive portfolio of software and tech assets acquired at 2020-2021 valuations that they cannot exit. Distributions to investors in 2024 were more than ten times lower than 2015 levels. The average holding period has stretched to 6.6 years. The 2020 and 2021 vintage funds, which deployed heavily into software during peak valuations, are showing DPI multiples of 0.30x and 0.20x respectively.

Those assets aren’t marked to market. They sit on PE fund balance sheets at manager-determined valuations that don’t get tested until there’s a transaction. When sponsors eventually have to refinance the debt on these companies, lenders will see what the business is actually worth in 2026 rather than what it was worth in 2021. Some PE owners will chip in more equity to protect their position. Others will look at a terminal software business and hand the keys to creditors.

Medallia is the case study. Taken private by Thoma Bravo for $6.4 billion in 2021. Struggling to service interest payments. Lenders potentially taking control. Roughly $5 billion of equity at risk. The Thoma Bravo fund that partially funded that deal has a 6.2% net IRR, bottom quartile for the 2020 vintage.

Multiply that across the industry’s software book and the numbers get large fast. Blue Owl’s Ostrover said it clearly: “If you’re worried about direct lending at all, you’ve got to be really worried about PE.”

The private credit stress is public because BDCs report NAVs quarterly and retail investors can request redemptions. The private equity stress is private because fund portfolios aren’t traded and LPs are locked in for a decade. Both are real. Only one is visible.

Blue Owl Has a Week to Breathe

It’s worth noting, fairly, that Blue Owl had a materially better week than the previous several.

PIMCO’s outright purchase of the $400 million Blue Owl Capital Corp bond was significant. It was the first BDC unsecured debt issuance in over a month and it cleared at terms that suggested genuine institutional demand rather than distressed pricing. The stock gained sharply over two days, outperforming Ares, Apollo and KKR.

Blue Owl’s GP Strategic Capital platform is also reportedly nearing a deal to take a minority stake in Paris-based BlackFin Capital Partners, a European financial services PE firm. That’s a business-as-usual GP stakes transaction of the kind Blue Owl has built a franchise around, and it signals the firm is still operating offensively in parts of its business even as the BDC redemption story dominates coverage.

The consensus analyst price target for Blue Owl sits at $14.07 against current trading levels near $9.65. That gap reflects either significant analyst optimism that hasn’t caught up to reality, or a market that has oversold the stock relative to fundamental value. Probably some of both.

One good week doesn’t resolve a 40% redemption request. But it changes the immediate narrative, and narrative matters in a market where retail investor behavior is driven as much by headlines as by credit fundamentals.

The Disclosure Reckoning Is Coming

The theme connecting everything this week is transparency.

Banks disclosing $180 billion in exposure. Adams Street calling for six new fund-level metrics. Apollo committing to monthly and eventually daily NAVs. Canada’s bank regulator restoring non-bank lending to its risk report. The Federal Reserve asking banks for private credit exposure details.

Every one of these moves is a response to the same problem. The private credit market grew to $1.8 trillion in a disclosure environment designed for a much smaller, purely institutional asset class. Retail investors got access to the returns without getting access to the information needed to evaluate the risks. Regulators are now trying to understand a market that moved faster than their data collection did.

Goldman’s Kristin Olson framed it charitably as “an education moment.” Jeff Diehl at Adams Street framed it as an unacceptable data void. Both are right.

The direction is clear regardless of framing. Disclosure standards will increase. The managers who get ahead of that voluntarily will be better positioned with both regulators and investors than those who wait to be pushed. The ones with portfolios that look better under additional scrutiny have an obvious incentive to move first.

The ones who don’t move first are telling you something too.

Where the Cycle Stands

The acute phase of the retail redemption crisis may be easing. The deeper structural problems are not.

Back leverage costs are rising and won’t come back down quickly. The $770 billion stress figure from Davidson Kempner is not a default forecast but it’s not nothing either. The maturity wall in software debt is a 2027 and 2028 problem that hasn’t started yet. The PE equity cushion that protects senior secured credit looks thinner the longer software valuations stay depressed.

What changed this week is that the banks showed their hand, partially and under pressure, and the number was large but not catastrophic. Markets took that as permission to exhale.

The exhale is probably warranted. The problems haven’t gone away. They’ve just moved from the acute phase, redemption panic and forced selling, to the chronic phase, back leverage compression, disclosure pressure, creeping soft defaults and a PE exit market that remains effectively closed.

Chronic is harder to trade. It’s also harder to ignore.